Accounting can seem complicated and it’s often difficult to navigate. We have created a short guide for you so that you can better understand what business accounting is all about and how to do it for yourself!

Why every self-employed, small businesses and SMEs need accounting

Proper accounting is not only useful, but is crucial for any business or self-employed person. Here are the benefits of business accounting:

- Informs you about the current or past financial performance of your professional activity.

- Allows you to analyze the financial situation, draw conclusions, make informed decisions and make forecasts.

- Be in good standing with the government regarding tax returns.

Business Accounting Concepts 101

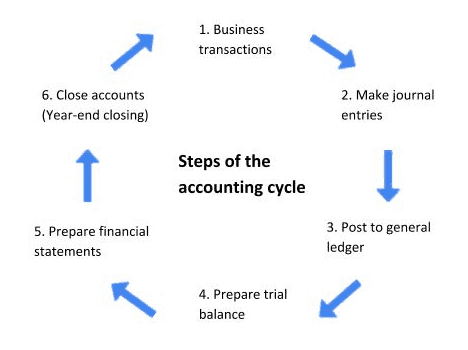

The accounting cycle

Cash and accrual accounting

In accrual accounting, transactions are recorded in accounting records when they occur or when invoices are issued. Accrual accounting does not take into account the date of collection.

As for cash accounting, it’s based on cash outflows and inflows. Transactions are recorded when cash is received from customers, and expenses are recorded when cash is paid to suppliers.

Accrual accounting is the generally accepted accounting method in Canada, except for a few types of businesses. Most self-employed workers must keep an accrual accounting.

Manage your business accounting: where to start?

In our article 7 Steps to Get Started with Your Business Accounting, we cover the basics of business accounting, which include:

- Creating a chart of accounts

- Open a company bank account

- Learn about sales taxes

- Determine how you want to get paid

Do your bookkeeping

Once you have organized the first steps of your business accounting, you will have to think about doing your bookkeeping.

Bookkeeping is the process of recording all cash inflows and outflows in financial records (general journal and general ledgers) and balancing them (trial balance).

Debit and credit in double-entry bookkeeping

Double-entry accounting means that each transaction is entered twice: one account is credited with a given amount and a second account is debited with an equivalent amount. Debits and credits balance each other out.

Bookkeeping is used to prepare the balance sheet and income statement, tax returns and other financial reports.

With an online accounting software such as Kiwili, it’s easy to automatically generate journal entries for each transaction. For example, when you issue an invoice, enter an expense, receive a payment, or any other transaction, the system generates a corresponding journal entry. These entries are entered in the general journal and general ledger, which will allow you to generate your financial statements.

Compare accounts with bank reconciliation

Usually done at the end of the month, bank reconciliation is a process used to ensure that the company’s books are in line with the bank statements. An accounting software allows you to import your bank statements and check line by line if the transactions have been recorded in the general journal. The bank reconciliation is not mandatory, but it allows to control the concordance of the data of the accounts and to make sure of the reality of the accounting situation.

Financial statements and tax season

Financial statements are structured information about transactions that occurred during a year. The purpose of a financial statement is to track the performance of a company over time and make informed business decisions.

The financial statements include:

- Income statement: provides information on how much money the company generates and spends.

- Balance sheet: provides information on what the company owns and how much it owes.

- Cash flow statement: provides information on all cash flows

- The appendix: supplements the figures in the balance sheet and the income statement.

Note that the cash flow statement and appendix may not be necessary, depending on your business and region.

The type of tax return to be filed and the documents to be provided depend on the legal structure of your business, so you should inquire about it. In Quebec, every business must produce its financial statements every year.

Legal obligations

Each company must keep up-to-date records in paper or electronic format. You must, according to the law, keep your papers and documents because they could be checked. The shelf life depends on the type of documents and your region.

Advantages of an accounting software

An accounting software like Kiwili has several advantages for the entrepreneur who wants to take charge of his accounting.

- Saves time since the information is entered only in a single software.

- Saves accountant fees.

- Reduces risk of error.

- Keeps track of transactions electronically.

- Automatically calculates taxes.

- Allows you to make financial forecasts and track cash flow easily.

- Automatically generates journal entries, general ledger, balance sheet, income statement and trial balance.

- Simplifies bank reconciliation.

Kiwili acts as a valuable asset for managing your business accounting and bookkeeping. You can be autonomous and have a good view of your finances at any time! However, it is important to consult an expert to make sure you set up your accounting properly and make good financial and business decisions.

Want more information and tips on business accounting? Read our blog post: 6 Tips for Managing Your Business Accounting Successfully.

Kiwili is an all-in-one business management software. It is at the same time an easy invoicing software, an accounting software, a CRM, a convenient project management tool and a time tracking software. Everything you need to manage your business like a pro!![]()