Self-employed or running a small business? You’ve probably found yourself pondering the world of accounts – and what exactly does bookkeeping consist of? Is it something we can do easily enough by ourselves, or is it best handled by an accountant?

In this post, we’re going to run through the basic principles of bookkeeping, and explain why it is so useful – in fact, you should make it top of your to-do list! Allow us to suggest some tools for getting it done independently and with ease, which as an entrepreneur, should be music to your ears!

Bookkeeping or Accounting?

It’s easy to get confused between bookkeeping and accounting. While both processes share some common elements, primarily that they’re both key components to your business, they actually come into play at different stages of the financial cycle.

Simply put, bookkeeping focuses more on administration and consistently recording daily transactions.

Accounting makes subjective assessments to produce financial models, based on bookkeeping records and other financial information, for advisory purposes to give insight into your business.

It is inevitable that there will be some crossover between these two roles, above all in a financially successful business, but generally speaking, bookkeeping is about helping to keep things organized while accounting provides analysis and consultation.

These days however, with the advent of online bookkeeping, accounting and business management software like Kiwili, small business owners and the self-employed are taking things into their own hands, taking care of everything from accounting, billing and invoicing to projects, time tracking and CRM with the help of these complete online solutions.

Books and Records for Small Businesses

Categorizing all of the incoming and outgoing payments is what’s referred to as bookkeeping, this is done in different classes of accounts and recorded in a general journal. The general journal is a continuous and chronological record of all financial transactions made by the company within a period often called the financial year. Making an entry in the books means logging at least two actions: a debit and a credit in the general journal. Note that in accounting, in a bank account, a receipt is recorded in debit and a withdrawal, in credit. It all comes down to a basic principle of double-entry accounting. That’s to say that there is always at least one posting line under debit and one under credit (but there can be a number of lines in debit and just one in credit for the same transaction, or vice-versa). In one entry, the amount of posting lines logged under debit must be equal to the amount of posting lines under credit. In accounting lingo, this means that the entry is balanced.

Example of a journal entry for receipt of a payment of a customer invoice amounting to $1732,11:

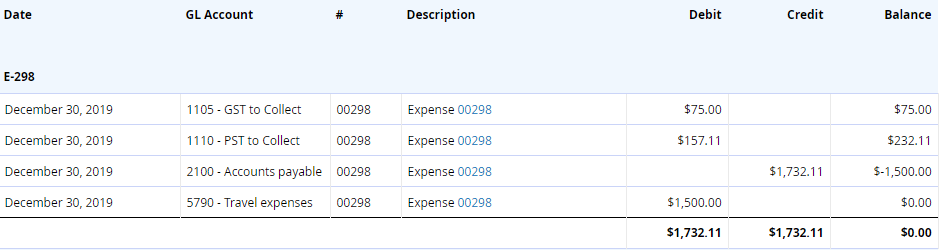

Example of an entry paying for an expense amounting to $1732,11:

In these examples, our accounting entries are balanced, as the total amounts in debit and credit are equal and the balance is therefore at $0. All the entries contained in the general journal will feed into the general ledger. The general ledger lists the same elements as the general journal, but in the general ledger they are also attached to their respective account. Here, more detail can be found on each entry and its impact on the corresponding chart of accounts. The accounts entries also go into the trial balance. A trial balance is quite simply a list of all the credit and debit balances from all your company’s accounts. This report is then used to check that there haven’t been any errors and that the total debited is equal to the total credited. The trial balance is usually prepared at the end of a financial period and is preliminary to the production of financial statements.

Bookkeeping for the Self-Employed

Those who are self-employed are required to have accounting entries in the form of a cumulative monthly register for income and expenditure, including the following supporting documents:

- Sales invoices

- Receipts for business expenses

- Bank statements

- Cheques

- Deposit slips, and more generally any documents that could account for a business expense

This evidence must be filed and stored for 6 years for purposes of possible accounts inspections.

Why Good Record-Keeping Matters

Updating your books regularly and efficiently is essential for any entrepreneur. Not only is proper bookkeeping a legal requirement that allows you to make accurate and timely payments, it also enables you to:

- Immediately detect discrepancies and disparities

- Monitor cash flow (liquidity)

- Avoid making mistakes and losing documentation

- Know the performance of your business in real time and in detail

- Ensure good business management and clear decision making

Handling Your Own Bookkeeping?

Being self-employed or a small business, using an accounting software is the simplest way to do your bookkeeping and accounting by yourself at a reduced cost, saving your hard-earned cash. With an online bookkeeping and accounting program such as Kiwili, all you need to worry about is making transactions (billing your clients and logging your expenses), and the platform will take care of generating journal entries for you, saving you time as a result, and also reducing your margin of error.

Verifying Your Accounting Records with Bank Reconciliation

Usually carried out at the end of the month, bank reconciliation is a process which is used to ensure that the company’s books tally up with the bank statements. An accounting software like Kiwili enables you to import your bank statements and check line by line that the transactions have been well-recorded in the general journal. Bank reconciliation is not mandatory, but it makes it possible to verify the consistency of accounts data and guarantee the reliability of the statement of accounts.

To summarize..

For best practice within your small business, it’s essential to work on both your daily bookkeeping and regular accounting. Remember that bookkeeping focusses on recording the day-to-day transactions of your company, whereas accounting is an assessment of your books and financial position more generally, primarily used for insight into your business and advisory purposes. Bookkeeping is simply keeping on top of your finances – and accounting is analysis.

In the past and to this day, businesses would employ a dedicated bookkeeper and accountant, however with the advent of online bookkeeping, accounting and business management software like Kiwili, these days people are taking things into their own hands, managing their finances independently from cradle to grave with the help of online solutions.

Sign up for Kiwili today for the best all-in-one management software for entrepreneurs and SME’s, and simplify the day-to-day management of your business.

Kiwili is an all-in-one business management software. It is at the same time an easy invoicing software, an accounting software, a CRM, a convenient project management tool and a time tracking software. Everything you need to manage your business like a pro!![]()